Egypt Edition

Egypt Edition  MENA+ Edition

MENA+ Edition  UAE Edition

UAE Edition  Saudi Edition

Saudi Edition  MENA <> India Corridors

MENA <> India Corridors  Logistics (MENA)

Logistics (MENA)  Climate (MENA)

Climate (MENA)

Share Issue

Share Issue

Good morning, wonderful people, and happy Wednesday. The ongoing power crisis is top of mind for us this morning as we contemplate when to take the elevator or the stairs at home and at work. Broadly speaking, though, things have been better in the past 48 hours than they were in the two days before that.

It’s Day 2 of the nationwide blackout schedule and it’s safe to say there have been a few teething problems: The first day of the government’s new system for organizing the ongoing rolling blackouts didn’t appear to go plan, according to what Lamees El Hadidi reported on the airwaves last night. Only a few areas around the country saw blackouts take place on schedule, with some reporting unexpected power cuts, others saying the blackouts lasted longer than an hour, and others still having had no cuts at all. Head to our talk show section below, for more.

GOOD NEWS- Our first shipment of mazut has arrived: The Electricity Ministry on Sunday received 35k tons of imported mazut to help fire the national electricity grid, a source at the ministry told us yesterday. That shipment has, together with a parcel of power-saving measures, allowed the Madbouly government to dial-down power cuts, our source said. The news was first picked up by Al Mal.

Remember: The shipment is the first of the government’s planned imports of the heavy oil so that it can ramp-up generation capacity to meet spiking demand. Prime Minister Moustafa Madbouly said last week that the government would spend USD 250-300 mn by the end of August on importing new supplies of mazut as part of a group of measures aimed at ending the power crisis. The state had stopped importing the heavy oil in March thinking that it could rely on local production during the summer and not anticipating the prolonged heat wave seen over the past weeks.

Gulf oil coming? The government has contracted with an unspecified Gulf country to source more supplies of mazut, according to Al Mal’s sources.

PSA #1- The mercury will peak at 37℃ during the day in the nation’s capital, dropping to 25℃ overnight, the Egyptian Meteorological Authority said yesterday . The 14-day forecast on our favourite weather app has the mercury at or above 40°C every day from tomorrow.

PSA #2- New government app aims to attract foreign investors: Cabinet has launched an English-language mobile app to showcase government efforts to improve the business environment and attract foreign investment, according to a ca binet statement yesterday. The app includes a guide to the Golden License system, as well as a section listing economic indicators, including growth rates, employment, and inflation. Get it here: iOS | Android.

HAPPENING TOMORROW-

PMI: S&P Global will publish its purchasing managers’ index for Egypt tomorrow. The non-oil private sector contracted at its slowest rate in 22 months in June amid signs at the time that inflationary pressures could be easing.

Interest rates: The Central Bank of Egypt is meeting tomorrow to discuss interest rates. All seven analysts and economists we spoke to think the CBE’s Monetary Policy Committee will keep rates on hold for a third consecutive meeting; some of those polled expect a a devaluation later this year. A Reuters poll also forecasts rates to remain unchanged.

National Dialogue: Participants at the National Dialogue will discuss a draft law establishing a new council for education and training and post-divorce issues.

IT’S A NEW MONTH: Other news triggers triggers to watch out for over the coming days:

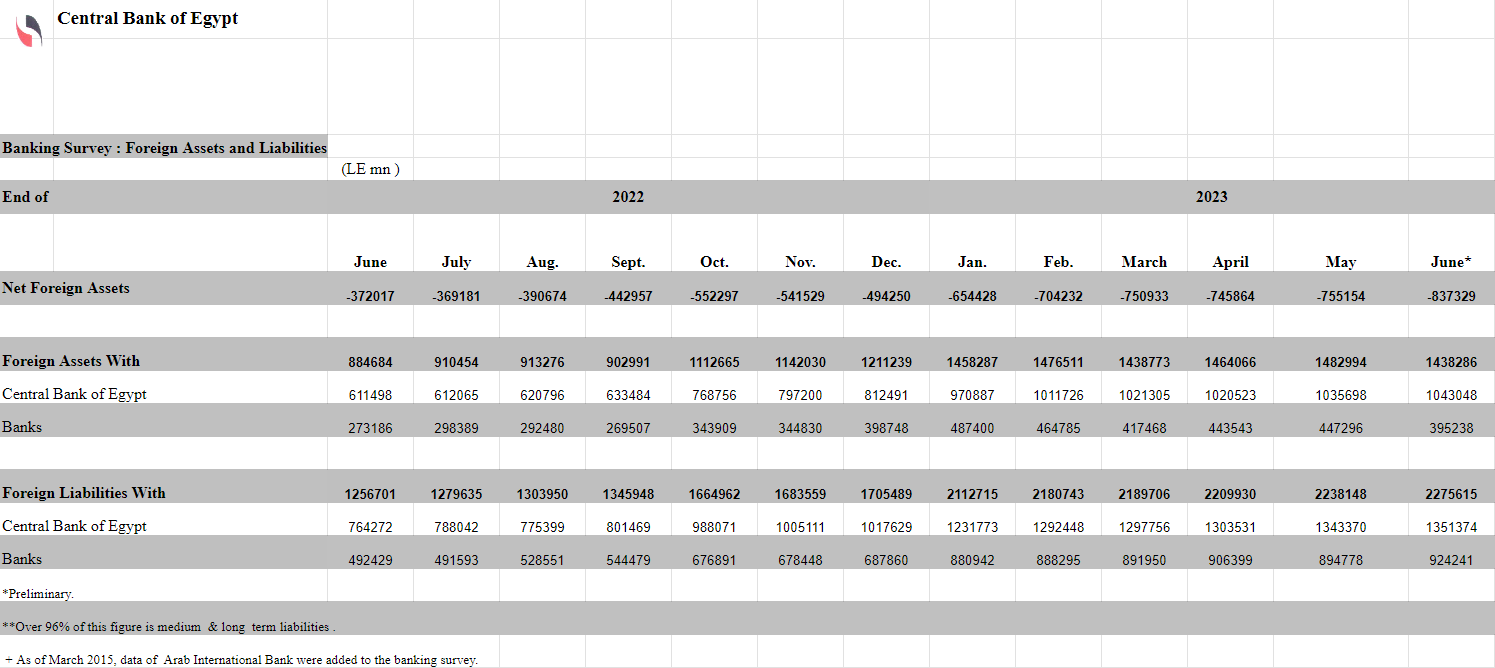

- Foreign reserves: The central bank will publish July’s foreign reserves figures at the end of this week or the beginning of the next. FX reserves continued to inch up in June, reaching USD 34.81 bn.

- Inflation: Capmas and the CBE will publish inflation figures for July on 10 August. Annual urban inflation hit a record high in June as the impact of multiple devaluations continued to feed through into the economy.

Check out our full calendar on the web for a comprehensive listing of upcoming news events, national holidays and news triggers.

THE BIG STORIES ABROAD-

There are two stories dominating the conversation in the Western press this morning:

#1- Donald Trump indicted (again): Agent Orange has been indicted for the third time in four months in connection with his attempts to overturn the 2020 election. The former president faces four charges including conspiracy to defraud the US, obstructing an official proceeding, and conspiring against the rights of voters.

Don’t expect this to make a difference to the polls: Trump’s overwhelming lead in the Republican primary polls has only grown with each indictment, and currently holds a huge 36-point l ead over faltering Trump Lite candidate Ron DeSantis. ( Associated Press | Reuters | Bloomberg | Financial Times | New York Times | Washington Post | Wall Street Journal | CNBC)

#2- The US just lost an A: Fitch downgraded the US sovereign credit rating from A AA to AA+ yesterday, citing expectations for fiscal pressure over the coming three years and the repeated high-stakes congressional battles over raising the debt ceiling. ( Associated Press | Reuters | Bloomberg | Financial Times | Washington Post | Wall Street Journal | CNBC)

Get Enterprise daily

The roundup of news and trends that move your markets and shape corporate agendas delivered straight to your inbox.

CIRCLE YOUR CALENDARS- The Enterprise Finance Forum is taking place on 18-19 September at the St. Regis Hotel in Cairo. This flagship forum is the latest in our must-attend series of invitation-only, C-suite-level gatherings that allow senior members of our community to openly and frankly discuss critical issues in key sectors of the economy.

TAP OR CLICK HERE if you want to express interest in attending. We’ll be sending out the first batch of invitations soon.

Do you want to become a commercial partner? Ping a note to Moustafa Taalab, our head of commercial, or fill out this form and we’ll be in touch.

*** It’s Hardhat day — your weekly briefing of all things infrastructure in Egypt: Enterprise’s industry vertical focuses each Wednesday on infrastructure, covering everything from energy, water, transportation, and urban development, as well as social infrastructure such as health and education.

In today’s issue: A new report says that private-sector real estate developers were working on residential and mixed-use projects worth c. USD 309 bn in 1Q 2023.

{kind=link}