We think Standard & Poor’s sovereign credit rating model breaks down when applied to Egypt — and that’s preventing an improvement in the rating agency’s outlook on Egypt and a possible upgrade in the credit rating. Why does this matter? Lower credit ratings translate into higher borrowing costs for the state and are a barrier to some investors. At the heart of it: S&P says, qualitatively, that it welcomes the float of the EGP, which it says will do good things for the economy going forward. But quantitatively, their model for assessing our credit rating punishes us for the magnitude of the very same devaluation they say they welcome, making it impossible for them to upgrade our credit rating or outlook. Contrast that with the exceptional performance of Egypt’s eurobonds in the market, which is arguably a real-world, fact-based argument in favour of an upgrade. Here’s the backstory, and how we think S&Ps model is holding Egypt back:

THE BACKGROUND: We spoke by phone with the S&P analyst responsible for Egypt’s credit rating on Monday to dig deeper into the drivers of the agency’s most recent report on the country, in which theyaffirmed Egypt’s credit rating at B- / Stable on 12 May. “Overall, the situation [in Egypt] is improving,” the credit analyst said. The stable outlook and affirmation of the rating are balanced out by risks arising from fiscal and external deficits and the gradual implementation of reforms. S&P sees GDP growth slowing down to 3.8% from 4.3% in the current fiscal year. That’s because devaluation of the EGP and the subsequent wave of high inflation are seen as weighing heavily on domestic demand, the main driver of economic growth over last years. Instead, foreign and domestic investment are likely to drive growth in the coming period, alongside net exports.

The ratings agency sees the Ismail government’s reforms starting to bear fruit in late2018 and early 2019. Economic growth in 2017 will take a hit as we adjust to the new foreign exchange regime and as inflation continues to be high. And presidential elections in 2018 are likely to cause investors to take a “wait and see” stance. These factors should dissipate by 2019 and, coupled with a rebound in tourism and the start of production from Zohr, should see GDP growth accelerate. S&P thinks the fiscal deficit will narrow to 7% by 2020, pulling general government debt to a declining path that should see it drop to 82% of GDP by 2020.

Before the 12 May report, S&P last looked at Egypt on 11 November 2016. Heading into our call on Monday, our primary question for S&P was how they view the reform measures taken since November, given the stable rating and outlook in their most recent assessment. We were also concerned with how the international bond market was pricing Egyptian debt, as it was cheaper than the higher-rated Nigeria and Ethiopia, for example, and very close to Jordan’s, which carries a significantly higher rating of BB-. (See our take on Ahmed Namatalla’s piece for Bloomberg, Egypt’s performance on the bond market merits a credit upgrade.)

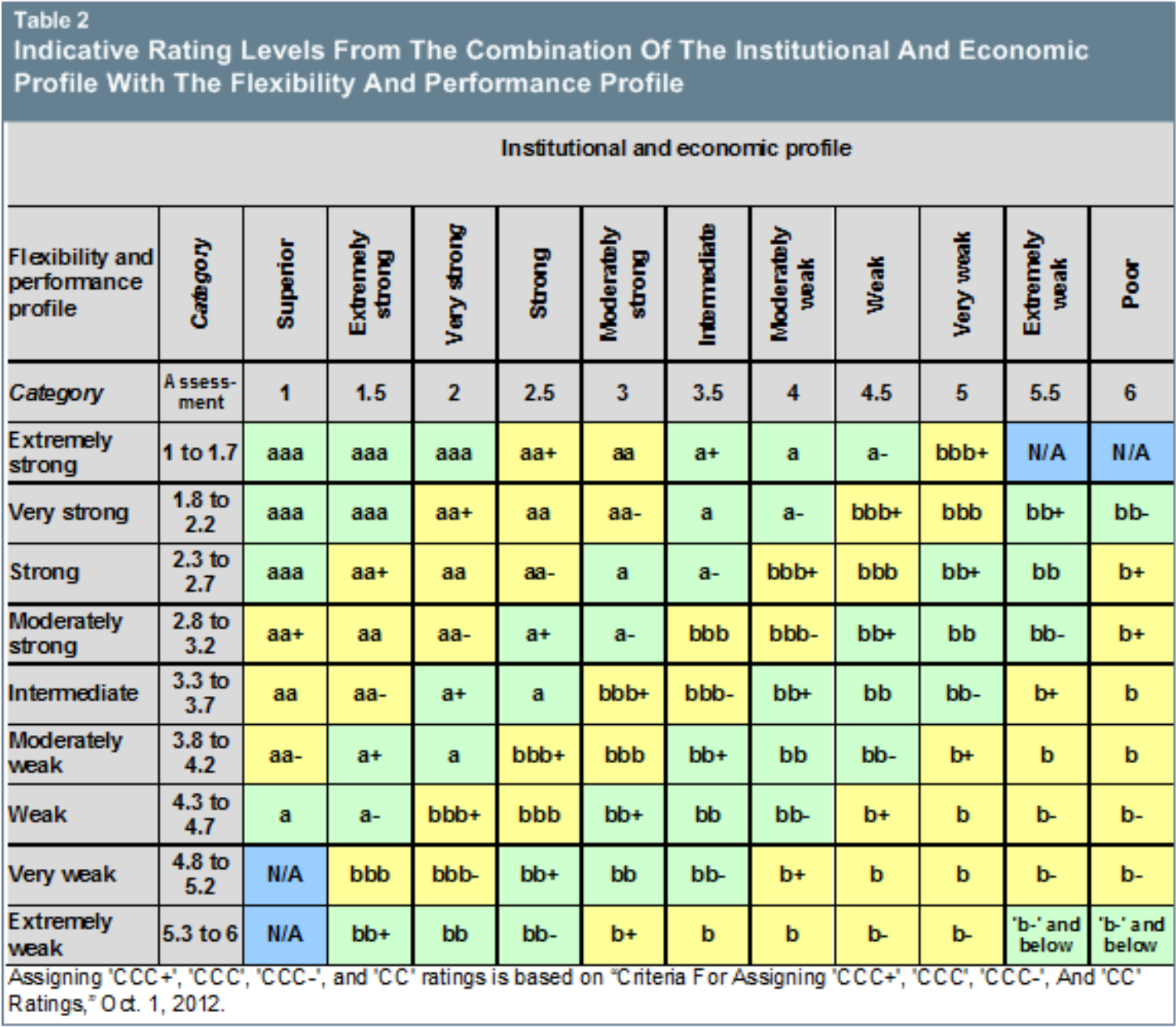

THE METHODOLOGY: This is where we need to get down into the weeds, so bear with us. The sovereign credit analyst explained that S&P’s sovereign credit ratings are driven by five factors that determine credit worthiness: institutional, economic, external, fiscal, and monetary. Together, they provide a sovereign indicative rating level that could then be subject to supplemental adjustment factors and “one notch of uplift / downlift, if applicable.” Each factor is given a score of 1 (strongest) to 6 (weakest). The institutional and economic assessments are averaged to give “the institutional and economic profile,” while the other three factors are averaged to give “the flexibility and performance profile.” The two profiles are used to determine an indicative rating level (specified in a table by S&P) with other factors that allow for the “one notch higher or lower” movement.

S&P says Egypt’s rating was “constrained by wide fiscal deficits, high public debt,low income levels, and institutional and social fragility,” according to the report. The fiscal deficit, as noted, is on a downward trajectory, bringing down public debt with it, S&P says. The S&P analyst also said “our institutional assessment did not change from the last one in November 2016.”

THE PROBLEM: Look at the rating criteria and you’ll see that the factor that weighed most heavily on S&P’s assessment was our poor performance on GDP per capita, which is measured in USD terms. According to S&P’s figures, USD-denominated GDP per capita dropped to USD 2.9k in FY 2016-17 from a peak of USD 3.7k in FY 2015-16.

Looking at the data provided with the S&P report as well as the S&P Sovereign Rating Methodology, we take issue with the rating agency’s criteria and the model they use. On the economic assessment criteria, S&P says: “The determination of the economic assessment uses the current-year estimate for the GDP per capita from national statistics, converted to [USD].” S&P then considers the real GDP per capita growth trend for the decision to bump the economic assessment score “one category worse or better than the initial assessment.”

S&P uses the same criteria (quite transparently) across all of the sovereigns it rates. The problem is that the methodology is not necessarily reflective of reality in Egypt. According to S&P data, real GDP per capita growth in Egypt grew by 2.9% in FY 2015-16 and by 1.5% in FY 2016-17. At the same time, using the same data, we can see that GDP per capita in USD terms has decreased by nearly 22% between FY 2015-16 and FY 2016-17 and is expected to drop further still by almost 21% to USD 2.3k in FY 2017-18. Since S&P says real GDP per capita growth in Egypt is positive, the expected decreases are then driven entirely by the exchange rate adjustment. GDP, in USD terms, is bound to be significantly lower in FY 2016-17 than in previous years as the currency lost nearly half its value, a drop that is by no means equates to an equal erosion of wealth.

And since the model’s starting point is the USD-denominated GDP figure, it seems clear to us that the ratings framework used by S&P is not responsive to large exchange rate adjustments such as the one we’re living through today in Egypt. S&P described the float of the EGP as “a vital step toward alleviating Egypt's acute foreign currency shortage, eliminating the differential between the official and unofficial exchange rates and improving the country's export competitiveness.” But quantitatively, the rating model punishes us for the float in calculating the economic assessment criteria.

Fundamentally, this suggests there are two problems with the model S&P is using for its sovereign credit ratings: First, forcing the USD denomination. Second, aggregating across measures — using averages based on so few criteria can lead to having one outlier causing big shifts, even when it should not.

Our take:

- S&P’s sovereign credit ratings model is broken in the case of Egypt and susceptible to bias.

- The credit rating report issued on 12 May does not necessarily reflect the reality of the economic situation in Egypt, nor the nation’s creditworthiness.

- Future rating decisions will continue to be inadequate as long as the model’s shortcomings are not addressed.

Related

13 of 14 economists surveyed by Reuters see the Central Bank leaving interest rates on hold when it meets this coming Sunday. “There is no need to change interest rates given that monthly inflation indicates the impact of the foreign exchange and energy shocks has dissipated, and with a weak monetary policy transmission mechanism, a rise in interest rates would not curb inflation,” the newswire quotes Arqaam Capital economist Reham Al Desouki as saying. Overnight deposit rates are presently set at 14.75% while overnight lending rates are at 15.75%. The IMF has recently made rumblings about interest rates being the “right instrument” to manage inflation in Egypt. IMF boss Christine Lagarde has singled inflation out as one of Egypt’s biggest challenges at the moment.

Related

President Abdel Fattah El Sisi promised further personal tax exemptions and larger food subsidies to protect the low- and mid-income classes when he spoke to the editors in-chief of state-owned newspapers in his second interview with them this year. The government has plans to battle inflation and expand the social safety net to protect people from the effects of his administration’s economic reforms.

El Sisi gave props to Prime Minister Sherif Ismail for how the PM has steered the ship despite challenges and setbacks. El Sisi also said he was in constant contact with the government to ensure that things are moving according to plan. The president acknowledged that there are shortcomings, but said that they were all being systematically addressed one at a time. He also promised to submit a comprehensive statement out account early next year to compare Egypt now to when he first assumed office and assess how much had been achieved.

Before his time in office is up, El Sisi hopes to have completed most, if not all, the national projects that he promised people.

Other key takeaways from El Sisi’s interview:

- Egypt will save USD 3.6 bn a year once new gas fields come on stream next year, including Zohr, Atoll, and the East and West Delta concessions;

- The emergency law will remain in place and be enforced strictly and without compromise against anyone who threatens national security and stability;

- Ministries and other government offices will move to the New Administrative Capital by the end of 2018.

Related

Egypt is reaping the benefits of the Ismail government’s economic reform program, and the gains are clearest in the return of foreign investments and the increase in foreign reserves, World Bank MENA Vice President Hafez Ghanem said yesterday in an interview with ON Live. Further progress is contingent on continued inflows of investment that creates jobs and makes a dent in the unemployment problem — as well as on improving the country’s education system. Ghanem hinted that Egypt’s ranking in the World Bank’s Ease of Doing Business index will reflect positive developments such as the availability of FX following the EGP float. He also had plenty of nice things to say about the progress on the WB-funded rural sanitation project, including the high speed of implementation. You can watch the interview in full here (runtime 47:30).

Related

M&A WATCH- US investment fund Lincoln Investment, ACDIMA, and a Compass Capital fund are going head-to-head in a race to acquire United Pharma IV Solutions, Al Mal reports. Al Mal says Lincoln’s bid is in the EGP 450-540 mn range, while Compass Capital has offered EGP 450-500 mn, but negotiations are still ongoing. United Pharma favors ACDIMA as a suitor, as “a state company that would make IV solutions available in public hospitals,” Chairman Abdallah Mahfouz tells Al Mal.

Related

EARNINGS WATCH- Our friends at SODIC reported a 321% y-o-y increase in net profit to EGP 211 mn in 1Q2017. The increase came on a 275% y-o-y increase in revenues “reflecting the ramp up in delivered units. Revenues were bolstered by deliveries in Eastown Residences and Westown Residences that combined accounted to more than 80% of the delivered value.” SODIC also says it record a net profit margin of 30%, improving 300 bps from 1Q2016. Managing Director Magued Sherif commented on the results saying: “Our results for the quarter reflect our continuing growth momentum. The strong trust of our clients in the SODIC brand has driven sales growth despite economic headwinds. Driven by our unwavering commitment to delivery, our financial performance is reaping gains. Our excellence in execution is reflected in the strong revenue growth and is solidified by our healthy profitability.” Critically, net contracted sales (essentially the company’s pipeline of future revenues) were up 71% to EGP 1.2 bn in the first quarter.

Orascom Hotels and Development reported consolidated net profit of EGP 75.9 mn in 1Q2017 compared with a EGP 118 mn loss a year before, according to its earnings release. The company reported a 73.8% y-o-y increase in revenues to EGP 493.9 mn in 1Q2017.

Orascom Development Company reported a consolidated net loss of CHF 12.5 mn in 1Q17, compared with a net loss of CHF 31.9 mn in 1Q16, according to its earnings filing. Real estate revenues reached CHF 12.3 mn in 1Q17 compared with CHF 21.7 mn in 1Q16.

Crédit Agricole Egypt grew its net profit for 1Q2017 by 51.6% to EGP 457.1 mn, the bank’s Managing Director François Edouard Drion told the press on Tuesday.

Related

Education Ministry to announce caps on international school tuition fees: The Education Ministry is expected to announce a new system regulating tuition fees at international and private schools, Youm7 reports, citing unnamed ministry sources. According to the sources, Minister Tarek Shawki is refusing to allow schools to hike fees by 20% each year and will cap price increases at 7-15%. Schools will be evaluated individually and their quality will determine the maximum annual fee hike they’ll be permitted. International schools had said in January that they should be regulated by the Investment Ministry, rather than the Education Ministry, after Shawki’s predecessor El Hilali El Sherbini placed the International School of Choueifat and the American International School under administrative and financial supervision last year.

Related

DISTRACTIONS- Tech geeks who happen to worship at the temple of Apple will want to check out wunderkind Mark Gurman’s latest for Bloomberg, wherein he claims Apple will be refreshing the MacBook Pro, 12-inch MacBook and (just maybe) the MacBook Air at WWDC in a few short weeks’ time. Finance geeks will doubtless not be short of opinions on the notion that 2016 was the worst year for hedge fund pay since 2005, the Financial Times and New York Times report. And if our deep dive into S&P’s methodology isn’t enough for you, econogeeks will want to check out the FT’s piece on how demographics are going to hobble both Asia and Africa in the future. Asia could grow old before becoming rich, but Africa’s population growth may prevent it from ever becoming wealthy.

Related

Egypt Edition

Egypt Edition  MENA+ Edition

MENA+ Edition  UAE Edition

UAE Edition  Saudi Edition

Saudi Edition  MENA <> India Corridors

MENA <> India Corridors  Logistics (MENA)

Logistics (MENA)  Climate (MENA)

Climate (MENA)

Share Issue

Share Issue

{kind=link}